Pay Yourself First: The Simple Formula for Building Wealth

John Gatewood CFP® CLU® | Founder | Director of Advisor Development

01.01.25

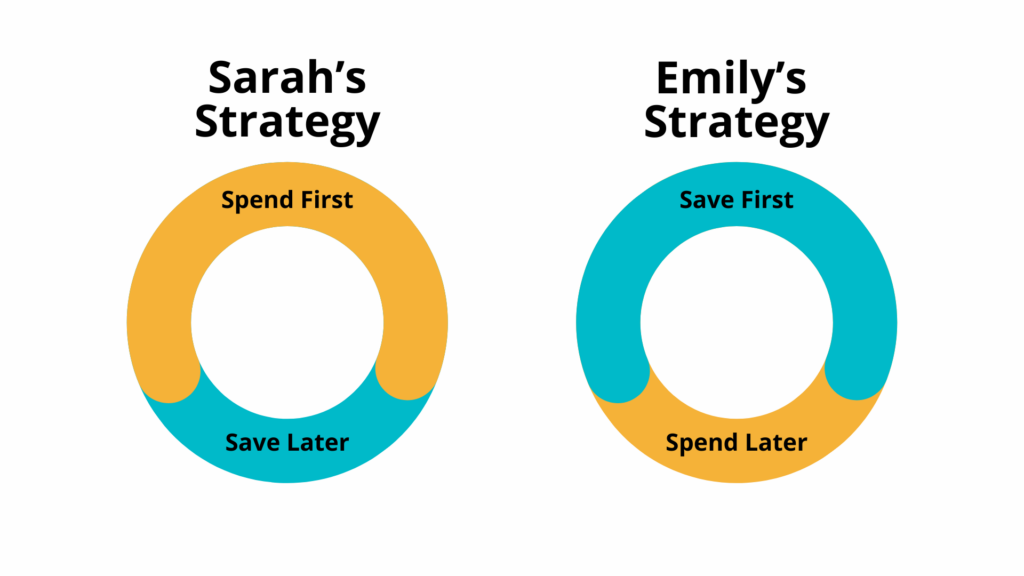

Meet Sarah. Sarah earns a strong income, has a well-documented budget, and keeps track of every dollar she spends. Yet, at the end of every month, she finds herself with little to show for her efforts. Bills pile up, unexpected expenses crop up, and her savings account barely moves. Despite her best intentions, Sarah feels like she’s treading water—always working hard but never truly getting ahead.

Now, meet Emily. Emily earns about the same as Sarah, but her approach is different. Rather than budgeting every expense down to the penny, Emily follows one simple rule: pay yourself first. Every month, Emily sets aside a fixed percentage of her income—without fail—into her savings and retirement accounts. Whatever is left, she uses for bills, discretionary spending, and fun. Unlike Sarah, Emily doesn’t stress about where every dollar goes because she knows her financial future is secure.

“Pay yourself first. Then pay everyone else.”

The Power of Paying Yourself First

The difference between Sarah and Emily isn’t income or discipline—it’s strategy. Paying yourself first is the cornerstone of financial success. It’s a simple shift in mindset: instead of saving what’s left after spending, you save first and spend what’s left. This approach helps ensure you’re building wealth systematically, rather than leaving it to chance.

Here’s why this strategy works:

Automated Success: By setting up automatic transfers to your savings or retirement accounts, you remove the temptation to spend the money elsewhere.

Freedom to Spend: When you’ve already saved, you don’t have to feel guilty about how you spend the rest. Whether it’s dining out, a spontaneous trip, or a new gadget, you’ve earned the right to enjoy your money.

Compound Growth: The earlier you start saving and investing, the more time your money has to grow. Small, consistent contributions today can turn into significant wealth tomorrow.

Why Budgets Often Fail

Budgeting can feel restrictive, and for many, it’s a system that’s easy to abandon. When you budget, you’re constantly making decisions about what to cut, which can lead to frustration and, ironically, overspending. Paying yourself first eliminates this decision fatigue. By prioritizing savings, you’re securing your future without obsessing over every expense.

Avoid the Interest Trap

There are two types of people in the world: those who earn interest and those who pay it. The “pay interest” group often spends first, saves whatever is leftover (if anything), and ends up relying on credit cards or loans to fill the gaps. This cycle of debt makes everything more expensive and creates a financial treadmill that’s hard to escape.

The “earn interest” group, however, saves first and lets their money work for them. They systematically invest, avoid unnecessary debt, and benefit from the power of compounding.

Building Wealth: The Core Principles

To position yourself for financial independence, follow these basic principles:

Live Below Your Means: Spend less than you earn, no matter your income level.

Pay Down High-Interest Debt: Attack high-interest debt like credit cards first, and free yourself from the burden of compounding interest.

Systematically Save: Set a savings goal—start with 10–20% of your income—and automate contributions.

Build an Emergency Fund: Aim for 3–6 months’ worth of expenses to cover unexpected events.

Max Out Retirement Accounts: Take full advantage of 401(k) plans, IRAs, or Roth IRAs for tax-advantaged growth.

Invest in a Diversified Portfolio: Use dollar-cost averaging to invest consistently in a balanced portfolio of stocks, bonds, and other assets. Avoid chasing high-flyers or timing the market.

The Bottom Line

Paying yourself first is the simplest and most effective way to build wealth over time. It shifts the focus from what you can’t spend to what you can save, creating a sense of freedom and confidence in your financial journey.

So, the next time you receive a paycheck, remember Emily’s example. Before you pay your bills, treat yourself—your future self, that is. Because true financial security begins with one simple act: paying yourself first.

"Our relationship with Gatewood Wealth Solutions has evolved over the years right along with our family. From building and protecting our wealth to retirement and estate planning, Gatewood has guided us and enabled our objectives. It’s assuring to know skilled professionals we trust are working with us to optimize what we have worked for all our lives."

"My wife and I have had the benefit of working with John Gatewood for over thirty-five years. Initially, John worked with us planning our personal and business life insurance needs. As his service offerings expanded, we took advantage of his expertise to help us with our family's financial planning. We could not be more pleased than what we are with the plan the Gatewood Wealth Solutions team developed for us. The team members are well-trained, intelligent, friendly, enthusiastic, and very good listeners. We have two scheduled reviews of the plan every year with one of the principals and at least…"

"My wife and I have known and worked with John Gatewood and his team for nearly a decade. The values-driven team of Gatewood Wealth Solutions is motivated, caring, highly competent and personally fueled by character and integrity. I recommended Gatewood to friends and family - including my children - because their deep desire to help clients 'give purpose to their wealth' gives us all the opportunity to better serve our families and communities."

"Navigating the complexities of my corporate life was already a challenge, but when my husband passed away, it felt like an insurmountable mountain of emotions and paperwork. The team at Gatewood Wealth Solutions stepped in with compassion, efficiency, and expertise, guiding me through the entire estate settlement process. Their unwavering support made a world of difference during such a challenging time. I am profoundly grateful for all they've done and continue to do for me. Their services are truly unparalleled, and I wholeheartedly trust and recommend them."

"My wife and I became a client of Gatewood Wealth Solutions twelve years ago on the recommendation of a friend who was also a Gatewood client, and I am very glad that we did. Until that time, I had managed our 401(k) and investments, but with retirement on the horizon, we felt it important to get professional help for retirement planning and investment management. The Gatewood team developed an integrated financial and retirement plan that we refined together. It was based on information such as our current financial position, desired retirement date and lifestyle, anticipated job and retirement income, expenses,…"

"I have worked with Gatewood Wealth Solutions since its inception and could not speak more highly of my experience. Gatewood Wealth Solutions provides comprehensive wealth management services for my family in a very sophisticated way. Their planning services are comprehensive and consider all assets of our family, not just what they manage. This is important for our family since we have a real estate business which must be considered in our planning. They also help us with our estate and tax planning each year. Their service is exceptional and is proactive and not reactive. I have referred members of my…"

"I’ve been with Gatewood Wealth Solutions and its predecessor for 21 years as our financial advisors. I first met John Gatewood in 2002 when I purchased a life insurance policy from him when he was with Northwestern Mutual. Shortly after having additional discussions with John, we started using them as our only financial advisors. They continued over the years to more than perform above my expectations and also started to bring in additional talent within their organization in order expand and meet client’s expectations. Since they’ve organized as Gatewood Wealth Solution and separated from Northwestern Mutual, they’ve continued to add…"

"I have been with Gatewood Wealth Solution for seven years, and I would highly recommend them for wealth management services. They are a very efficient, effective, knowledgeable team that provides highly personalized, client-centered services. If I didn't know better, I would think that I am their only client! They have an excellent working relationship with a highly respected law firm that provides assistance with trusts and estate planning. They also have an excellent working relationship with a tax accounting firm. All of this so that all aspects of my financial planning needs are seamlessly coordinated. Their quarterly meetings are well…"

"Partnering with Gatewood Wealth Solutions has been one of the best decisions we have made in the last five years. I have met with numerous financial planners who’ve all come to me with similar ideas and recommendations that don’t seem to prove that they are thinking outside the box for me individually. But when Gatewood came to me with their plan it was strategically designed with so many aspects taken into consideration that I was surprised at how uniquely competent and professional they were. They brought me many ideas and recommendations that would not bring them profit. They brought me…"

"Gatewood Wealth Solutions gives me confidence that my retirement savings are being monitored and managed with MY best interest in mind. All of the staff is welcoming, friendly and respectful. They have comprehensive knowledge of long-term financial planning, estate planning and tax planning. I have been with Gatewood for many years and hope to be with them for many more years to come."

"I have known John Gatewood, the founder of Gatewood Wealth Solutions, for many years. We became friends well before we talked about business, and it was a natural decision to turn to John for help with our affairs when I needed it because I had grown to know and trust him. It really is true that John and his team at Gatewood Wealth Solutions are completely focused on helping ordinary families like ours to become financially independent. The family part especially means something: One day my 20-something son called to ask if I thought our group would be willing to…"

The statements provided are testimonials by clients of the financial professional. The clients listed have not been paid or received any other compensation for making these statements. As a result, the client does not receive any material incentives or benefits for providing the testimonial. These views may not be representative of the views of other clients and are not indicative of future performance or success.